Tax season creates predictable cash flow challenges for thousands of Canadians every year. Whether you’re waiting on a tax refund, facing an unexpected assessment, or managing the timing gap between business expenses and revenue, a tax season cash flow loan offers a targeted solution to bridge these temporary shortfalls.

These short-term financing options help you cover immediate expenses like rent, utilities, or payroll without depleting savings or missing critical payments. Understanding how they work is essential: tax season cash flow loans typically provide quick access to funds, often within 24 hours, with repayment structured around your expected income or tax refund timeline.

The key is matching the right loan to your specific situation. Individuals awaiting refunds might need smaller amounts for 2-4 weeks, while small business owners navigating quarterly tax obligations may require larger sums with flexible repayment terms. Responsible borrowing means calculating exactly what you need, confirming you can repay on schedule, and comparing options to find reasonable rates.

Canadian Payday Loan Advisors connects borrowers with trusted lending partners who understand tax season pressures. By evaluating your circumstances and explaining terms clearly, we help you make informed decisions that solve immediate cash flow problems without creating long-term financial strain. Smart planning today prevents difficult choices tomorrow.

Why Tax Season Creates Cash Flow Problems

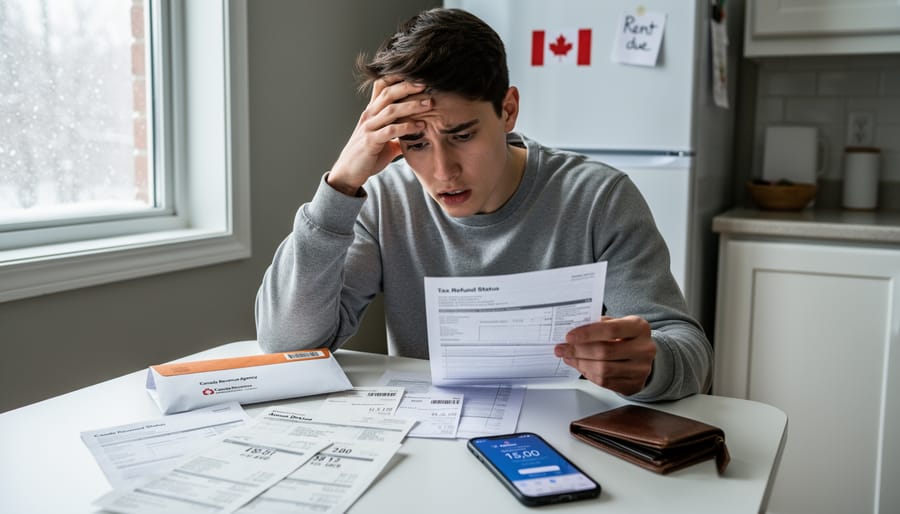

The CRA Refund Waiting Game

When you file your taxes with the Canada Revenue Agency (CRA), patience becomes part of the process. Most Canadians can expect their refund within two weeks when filing electronically, or up to eight weeks for paper returns. However, these are best-case scenarios that don’t always reflect reality.

Several factors can extend your waiting period considerably. If the CRA selects your return for review, requires additional documentation, or identifies discrepancies that need clarification, processing times can stretch for weeks or even months. First-time filers, those claiming new credits, self-employed individuals with complex returns, or anyone who owes previous debts to the CRA often face longer delays.

For many Canadians, waiting simply isn’t an option. Rent comes due, utility bills arrive, and business expenses don’t pause while the CRA processes paperwork. A single parent managing household expenses can’t tell their landlord to wait another month. Similarly, a small business owner facing inventory purchases or payroll obligations needs access to funds now, not later.

This timing gap between filing your return and receiving your refund creates genuine financial strain, making short-term lending solutions a practical bridge during tax season.

When Tax Preparation Costs Add Up

Tax season brings more than just filing deadlines—it often means paying upfront for professional services before you receive your refund. Many Canadians face accounting fees ranging from $150 to $500 for individual returns, while small business owners can expect costs between $500 and $2,000 depending on complexity. These expenses don’t wait for your refund to arrive, creating an immediate cash need.

Professional tax preparers typically require payment upon completion of your return, and gathering necessary documents may involve additional costs like requesting records from financial institutions or previous accountants. For self-employed individuals, quarterly installment payments add another layer of financial pressure during an already expensive time.

When these upfront costs strain your budget, a short-term loan can bridge the gap between paying for tax services now and receiving your refund later. This approach lets you access professional expertise without compromising your day-to-day expenses or dipping into emergency savings meant for unexpected situations.

What Are Tax Season Cash Flow Loans?

How They Work in Canada

Accessing a tax season cash flow loan in Canada is straightforward. First, you’ll identify a reputable lender who offers these specialized short-term loans. The application process typically requires basic personal information, proof of income, and details about your expected tax refund or seasonal revenue pattern.

Most lenders can process applications within 24 to 48 hours, with some offering same-day approval for urgent situations. Loan amounts generally range from $500 to $15,000, depending on your financial profile and the lender’s criteria. Businesses may access higher amounts based on their cash flow history.

Repayment terms are designed around tax season timing, typically spanning 30 to 90 days. Many lenders structure repayment to coincide with when you receive your tax refund or when your business cash flow improves after tax payments. Some offer flexible repayment schedules that accommodate your specific situation.

When applying, expect the lender to review your credit history, though many specialize in serving Canadians with various credit backgrounds. Interest rates and fees vary, so comparing multiple offers helps you find the most affordable option. Financial tip: Only borrow what you genuinely need and confirm you can comfortably repay within the agreed timeframe to avoid additional costs.

Who Benefits Most From These Loans

Tax season cash flow loans work particularly well for specific groups of Canadians who face unique financial timing challenges. Self-employed professionals often benefit most, as they typically wait months for client payments while facing immediate tax obligations. Small business owners juggling inventory costs, payroll, and tax payments find these loans bridge critical gaps between revenue cycles.

Contractors and freelancers who experience irregular income patterns are ideal candidates, especially when quarterly tax installments come due before project payments arrive. Seasonal workers—from tourism operators to agricultural businesses—can manage off-season tax bills without depleting reserves needed for operational restart.

Those managing both personal and business finances benefit significantly, particularly when coordinating business banking essentials with tax deadlines. Additionally, entrepreneurs experiencing rapid growth who need cash for expansion while meeting tax obligations find these loans valuable.

If your income doesn’t align neatly with traditional employment patterns, or you’re navigating the complexity of business ownership during tax season, these specialized loans offer tailored support. The key is ensuring your situation involves temporary timing issues rather than fundamental financial instability, making repayment realistic once your expected funds arrive.

Smart Ways to Use Tax Season Loans

Covering Tax Preparation and Filing Costs

Professional tax preparation services can range from a few hundred to several thousand dollars, depending on your situation’s complexity. While these services often result in larger refunds or valuable deductions that offset their cost, the upfront expense can strain your budget when bills are already piling up.

A tax season cash flow loan offers a practical solution. Instead of skipping professional help or draining your emergency savings, you can cover your accountant’s fees immediately and repay the loan once your refund arrives. This approach ensures you benefit from expert guidance without compromising your financial safety net.

When using loans for tax preparation costs, calculate the total expense before borrowing. Include consultation fees, document preparation charges, and any additional services you might need. Borrow only what’s necessary and have a clear repayment plan aligned with your expected refund date. This strategic approach helps you access professional expertise while maintaining financial stability throughout tax season.

Managing Unexpected Tax Bills

Receiving an unexpected tax bill from the CRA can feel overwhelming, but taking quick action helps you avoid mounting penalties and interest charges. The CRA applies compound daily interest on unpaid balances, which means delays cost you more over time. A tax season cash flow loan provides immediate funds to settle your tax debt, stopping additional penalties from accumulating while you manage repayment on more predictable terms.

Consider bridge financing as a strategic tool rather than a last resort. By paying the CRA promptly with loan funds, you maintain a positive standing with the tax agency and prevent collection actions that could impact your credit. The key is comparing the loan’s interest rate against CRA’s penalties to ensure you’re making a financially sound decision. Many Canadians find short-term loans offer breathing room to reorganize their finances without the stress of government debt collectors, allowing them to focus on long-term financial stability instead of crisis management.

Keeping Your Business Running Smoothly

Tax season often creates a perfect storm for Canadian businesses: significant tax payments come due just as you need to maintain regular operations. A tax season cash flow loan can bridge this gap, ensuring you meet critical business obligations without disruption. Use these funds strategically to cover payroll so your team stays motivated and secure, maintain supplier payments to preserve valuable relationships and avoid late fees, and handle day-to-day operational expenses like rent, utilities, and inventory replenishment.

When applying for business-focused loans, lenders will evaluate your company’s financial health differently than they would for consumer lending. Understanding the distinction between personal versus business credit helps you prepare stronger applications and access better terms. Keep detailed records of how tax obligations impact your cash position, as this documentation supports your loan request and demonstrates responsible financial management to potential lenders.

What to Consider Before Applying

Understanding Costs and Terms

Before committing to a tax season cash flow loan, it’s essential to understand exactly what you’ll pay. Interest rates on short-term loans typically range higher than traditional bank loans, reflecting the faster approval process and flexible requirements. Most lenders charge a flat fee based on the amount borrowed, often expressed as a cost per $100 borrowed.

For example, borrowing $500 might cost you $15-$25 per $100, meaning your total repayment could be $575-$625. Always ask for the annual percentage rate (APR) to compare options fairly across different lenders.

Repayment schedules usually align with your next payday or expected tax refund date, typically within two to four weeks. Some lenders offer installment options that spread payments over several months, which can ease the burden but may increase total costs.

Watch for additional fees like administrative charges, late payment penalties, or non-sufficient funds fees. Reputable lenders will provide a clear breakdown upfront showing the borrowed amount, all fees, total repayment amount, and due date. This transparency helps you make an informed decision and plan your budget accordingly. Never sign without understanding your complete financial obligation.

Your Repayment Strategy

Before taking out a tax season cash flow loan, create a clear repayment plan. Start by estimating when your tax refund will arrive—typically within two weeks if filed electronically. Use this timeline to determine your loan repayment date and ensure the borrowed amount aligns with your expected refund or upcoming income. Build a realistic budget that accounts for the loan repayment along with your regular expenses. Consider setting aside a small buffer in case your refund is delayed or smaller than anticipated. If possible, arrange automatic payments from your bank account to avoid missing deadlines and incurring additional fees. Remember, borrowing only what you need and can comfortably repay helps you maintain financial stability beyond tax season.

How Canadian Payday Loan Advisors Makes the Process Simple

Canadian Payday Loan Advisors understands that tax season financial challenges require fast, flexible solutions tailored to your unique situation. Rather than offering a one-size-fits-all approach, the company takes time to understand your specific cash flow needs and circumstances before recommending the right lending option.

The process begins with a simple conversation. Whether you need funds to cover an unexpected tax bill, bridge the gap until your refund arrives, or maintain business operations during slower periods, Canadian Payday Loan Advisors connects you with lending partners who specialize in tax season solutions. This strategic network of trusted lenders means you gain access to multiple options without navigating the complex financial landscape alone.

Quick approvals set this approach apart. Understanding that tax deadlines don’t wait, the company prioritizes efficiency without sacrificing personalized service. Most applicants receive decisions within hours, and approved funds can often be deposited the same day or next business day.

Throughout the process, transparency remains central. You’ll receive clear explanations of loan terms, repayment schedules, and associated costs upfront, ensuring no surprises down the road. The team also provides practical financial tips to help you manage repayment effectively and strengthen your financial position beyond tax season.

This customer-centric model transforms what could be a stressful borrowing experience into a straightforward solution, giving you the breathing room needed to navigate tax season confidently while maintaining your financial stability.

Alternatives to Tax Season Cash Flow Loans

Before committing to a tax season cash flow loan, consider these alternatives that might better suit your financial situation.

CRA Payment Arrangements offer flexible payment plans directly through the Canada Revenue Agency. You can negotiate terms based on your ability to pay, often without interest charges if arranged promptly. The main drawback is that penalties may still apply, and approval isn’t guaranteed for all situations.

Personal Lines of Credit typically provide lower interest rates than short-term loans, making them cost-effective for managing tax obligations. If you have good credit, this option offers flexibility to borrow only what you need. However, approval can take time, and rates vary significantly based on your credit profile.

Credit Cards can provide immediate access to funds, especially if you have available credit. Some cards offer promotional interest-free periods, which could work if you can repay quickly. Watch out for high interest rates after promotional periods end and potential cash advance fees.

Family Loans present an interest-free or low-cost borrowing option. This personal approach avoids credit checks and formal applications. However, mixing money with family relationships requires careful consideration and clear repayment agreements to prevent misunderstandings.

For businesses specifically, working with an accounting company can help you better forecast tax obligations and avoid future cash crunches. Additionally, focusing on building business credit creates more borrowing options for future tax seasons. Each alternative carries unique advantages and limitations, so evaluate them against your specific financial circumstances and repayment capability.

Financial Tips for Next Tax Season

The best way to avoid cash flow stress during tax season is to prepare throughout the year. By implementing a few strategic habits now, you can reduce or eliminate the need for loans when your next tax bill arrives.

Start by setting aside funds monthly specifically for taxes. If you’re self-employed or have variable income, aim to reserve 25-30% of your earnings in a separate account. This simple practice ensures you’ll have resources available when tax time comes, eliminating last-minute scrambling for funds.

Maintaining organized records throughout the year makes tax preparation smoother and helps you identify potential deductions. Keep digital copies of receipts, invoices, and expense reports in clearly labeled folders. Good recordkeeping not only reduces stress but can also lower your tax burden by ensuring you don’t miss eligible write-offs.

Consider quarterly tax planning sessions, either independently or with a financial professional. Reviewing your income and expenses every three months allows you to adjust your savings strategy and anticipate your tax obligations. This proactive approach through smart financial planning prevents surprises when filing deadlines arrive.

Building an emergency reserve separate from your tax fund provides additional security. Aim for three to six months of essential expenses in an accessible savings account. This buffer protects you not just during tax season, but throughout the year when unexpected costs arise.

If you’re a business owner, explore making voluntary quarterly tax payments to the Canada Revenue Agency. Spreading payments throughout the year improves cash flow management and reduces the financial impact of annual filing.

These strategies require discipline but deliver peace of mind. By planning ahead, you’ll face next tax season with confidence rather than financial anxiety.

Tax season doesn’t have to mean financial stress. While careful planning and budgeting throughout the year remain your best defense against cash flow challenges, tax season cash flow loans offer a practical safety net when unexpected gaps arise. These short-term financial solutions can help you meet immediate obligations, whether that’s covering personal expenses while waiting for your refund or maintaining business operations during a slower period.

The key to using these loans responsibly lies in understanding your repayment capacity and borrowing only what you genuinely need. Take time to compare options, read the terms carefully, and ensure the loan fits within your overall financial picture. Remember that these tools work best for temporary situations rather than long-term financial solutions.

Canadian Payday Loan Advisors is here to support you through tax season and beyond with transparent, accessible lending options tailored to your needs. By combining smart financial planning with the right resources when you need them, you can take control of your tax season finances with confidence. Whether you’re an individual waiting on a refund or a business managing seasonal fluctuations, the right approach and support can make all the difference in navigating this challenging time successfully.